The Ins And Outs Of House Mortgages

simply click the up coming article create by-Arsenault Breen

How is mortgage defined? A home loan helps to get you into a new home, and it's secured by the home you buy itself. If you are unable to pay for it, the bank will foreclose on it. This is a big responsibility, but the tips below can help you through it.

Consider the Federal Housing Authority to be your first stop when looking for a new mortgage. In https://www.cnbc.com/2021/05/18/jpmorgan-chase-names-two-women-executives-to-lead-consumer-bank.html , a mortgage with the FHA will mean putting a lot less money down. If you opt for a conventional loan, you will be required to come up with a serious down payment, and that can mean not being able to afford the home you really want.

If you are considering quitting your job or accepting employment with a different company, delay the change until after the mortgage process has closed. Your mortgage loan has been approved based on the information originally submitted in your application. Any alteration can force a delay in closing or may even force your lender to overturn the decision to approve your loan.

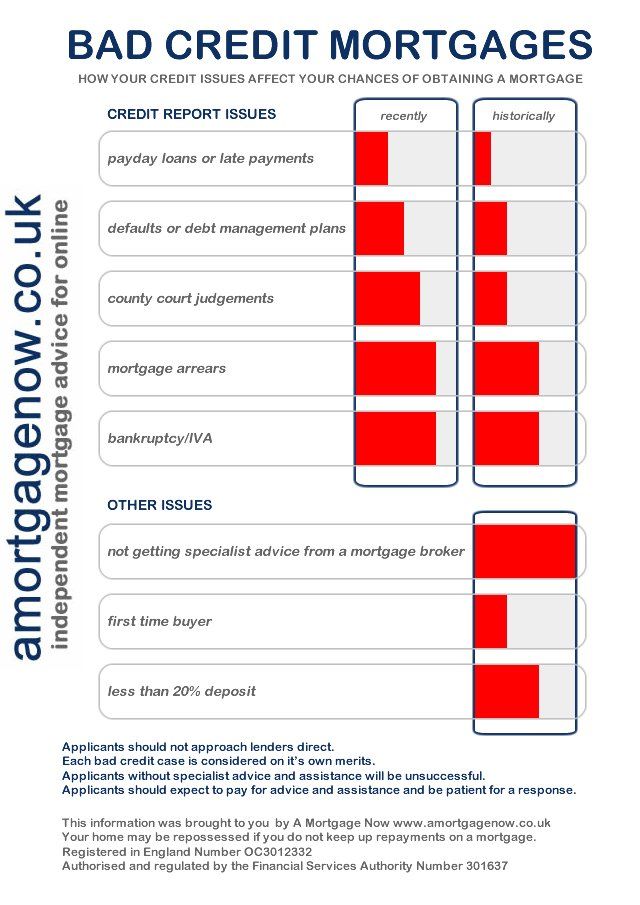

Consider investing in the services of a professional when you're about to take out a mortgage. There is much information to learn before you get a home mortgage, and the consultant can guide you to getting the best deal. They'll also check out the terms to ensure that they are in your favor as well.

Reducing your debt as much as possible will increase your chances of being approved for a mortgage. If you are not in a good financial situation, meet with a debt consolidation professional to get out of debt as quickly as possible. You do not need to have a zero balance on your credit cards to get a mortgage but being deeply in debt is definitely a red flag.

Start saving all of your paperwork that may be required by the lender. These documents include pay stubs, bank statements, W-2 forms and your income tax returns. Keep these documents together and ready to send at all times. If you don't have your paperwork in order, your mortgage may be delayed.

What do you do if the appraisal does not reflect the sales price? There are limited options; however, don't give up hope. You can dispute the appraisal and ask for a second opinion; however, you will need to pay for the appraisal out of your pocket at the time of the appraisal.

Try going with a short-term loan. Since interest rates have been around rock bottom lately, short-term loans tend to be more affordable for many borrowers. Anyone with a 30-year mortgage that has a 6% interest rate or higher could possibly refinance into a 15-year or 20-year loan while still keeping their the monthly payments near around what they're already paying. This is an option to consider even if you have slightly higher monthly payments. It can help you pay off the mortgage quicker.

Speak with many lenders before selecting the one you want to borrow from. Ask family and friends about their reputation, their rates and about any of their hidden fees they have in their contracts. When you have all the details. you can select the best one.

If you can afford the higher payments, go for a 15-year mortgage instead of a 30-year mortgage. In the first few years of a 30-year loan, your payment is mainly applied to the interest payments. Very little goes toward your equity. In a 15-year loan, you build up your equity much faster.

Know that Good Faith estimates are not binding. These estimates are designed to give you a good idea of what your mortgage will cost. It should include title insurance, points, and appraisal fees. Although you can use this information to figure out a budget, lenders are not required to give you a mortgage based on that estimate.

Know your mortgage interest rate type. When you are obtaining home financing you should understand how the interest is calculated. Your rate could be fixed or it could be adjustable. With fixed interest rates, your payment will usually not change. Adjustable rates vary depending on the flow of the market and are variable.

When rates are near the the bottom, you should consider buying a home. If you do not think that you will qualify for a mortgage, you should at least try. Having your own home is one of the best investments that you can make. Quit throwing away money into rent and try to get a mortgage and own your own home.

Be aware that certain things may need to be done to the property before the loan can be approved. One such thing is extra insulation added to the home. This work can either be done by the home buyer or the homeowner. However, once the work is completed, it must be inspected by a certified inspector.

Reduce your outstanding liabilities as much as possible before applying for a home mortgage loan. It is especially important to reduce credit card debt, but outstanding auto loans are less of a problem. If you have equity in another property, the financial institution will look at that in a positive light.

Do not embark on the process of buying a home if you have just started a new job within the last year. The best home mortgage rates go to those that have been with a company for a number of years. Having a job for a short time is seen as a risk, and you will be the one to pay for it with a higher interest rate.

Look into foreclosed homes before you seek out properties that are brand new. Banks don't mind dealing with other banks, and they certainly prefer less expensive properties. If you can find a home that's offered for a great price, especially if the bank in question owns it, they will jump at the opportunity to have someone pick up the tab. It's a better option for them than auctions.

Be sure to get home insurance quotes before you sign a home mortgage contract. There are many factors that could lead to a very high insurance rate. You want to be sure that you can afford everything involved before you get yourself locked into a contract that could lead to financial disaster in the end.

Now that you've read over this advice, you are ready to get out there and find the right mortgage for your home. You don't want to dive into this situation without the proper knowledge. Instead, you want to be able to make rational decisions along the way and get into the mortgage vehicle that works with you.